Preface • Work summaryOver the past year, factors such as 4G densification, upcoming 5G commercial, data centers, and the digitization of industrial connectivity have contributed to the development of the global optical communications market.

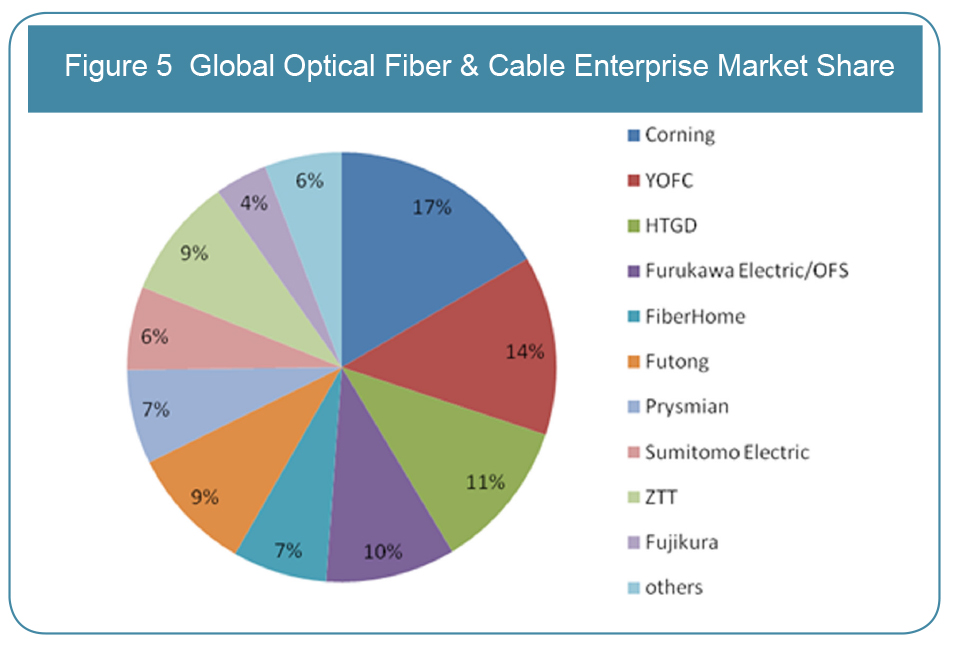

Network Telecom Information Research Institute has engaged in the competitiveness assessment of China/global optical fiber & cable enterprises for 12 years. “The Top 10 Competitiveness Enterprises in the Global Optical Fiber & Cable Field in 2018” clearly displays the competitive situations of main optical fiber & cable enterprises in 2018. The research shows that companies in top 10 competitiveness enterprises of global fiber & cable market list are divided up by four countries, namely, the United States (Corning), Italy (Prysmian), Japan (Furukawa Electronic/OFS, Sumitomo Electric, Fujikura) and China (YOFC, HTGD, FiberHome, Futong, and ZTT), with Chinese enterprises occupying half of the list. That is, YOFC ranks second in the world with 14% market share, while HTGD ranks third with 11% market share. FiberHome, Futong, and ZTT respectively ranks fifth, sixth and ninth with market share of 7%, 9% and 9%. Corning, Furukawa Electric/ofs, Prysmian, Sumitomo Electric, Fujikura take up market share of 17%, 10%, 7%, 6% and 4% respectively. These 10 enterprises entirely take up 83% of global optic fiber and cable market share, showing strong market competitive advantage.

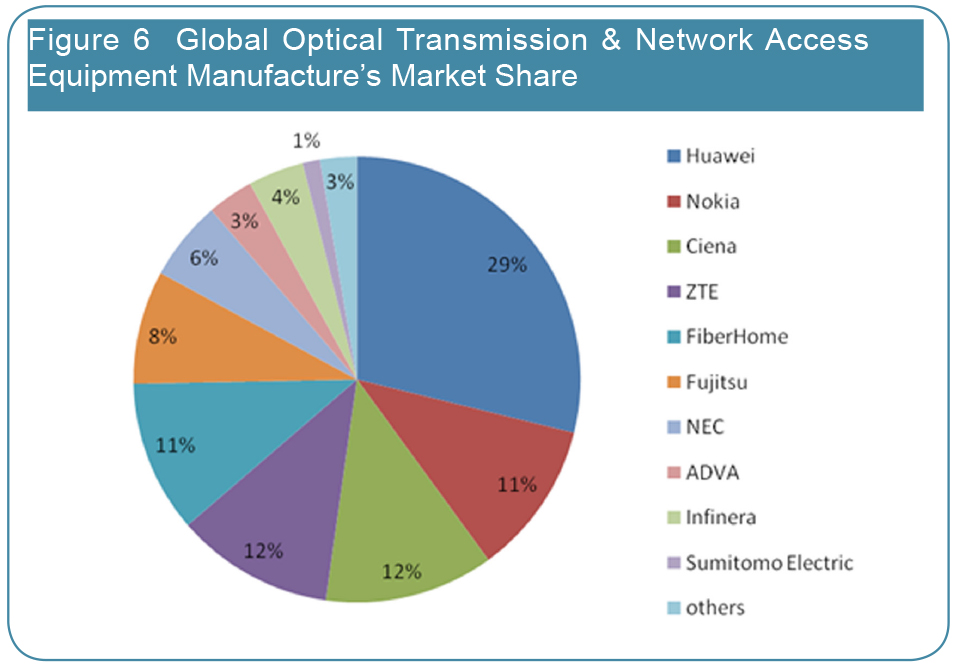

Viewing from the entire global optical transmission and network access equipment, HUAWEI stabilizes its leading position with competitiveness comprehensive score exceeding second Nokia of 69 points. Ten companies in this list come from five countries: Finland (Nokia), Japan (Fujitsu, NEC, Sumitomo Electric), the United States (Ciena, Infinera), China (Huawei, ZTE, FiberHome), and Germany's (ADVA). HUAWEI ranks first by sharing 29% of global optical transmission and network access equipment. Nokia locates number 2 with its 11% of market share. Ciena is listed number 3 with its 12% market share. ZTE is in number 4 location, with market share of 12%. And FiberHome is in number 5 location with its market share of 11%. Fujitsu, NEC, ADVANCE, Infinera, SUMITOMO ELECTRIC respectively take up 8%, 6%, 3%, 4% and 1% of market share. These 10 enterprises totally cover 97% of global optical transmission and network access equipment market share.

Optical network and transmission equipment is a sub-industry with high industrial centralization degree. In the last year, the five major equipment manufacturers’ revenue all realized positive growth. While on net profit aspect only Nokia showed loss situation. HUAWEI is the leader in this field, which has been listed 1st for many years, and is expanding its advantages.

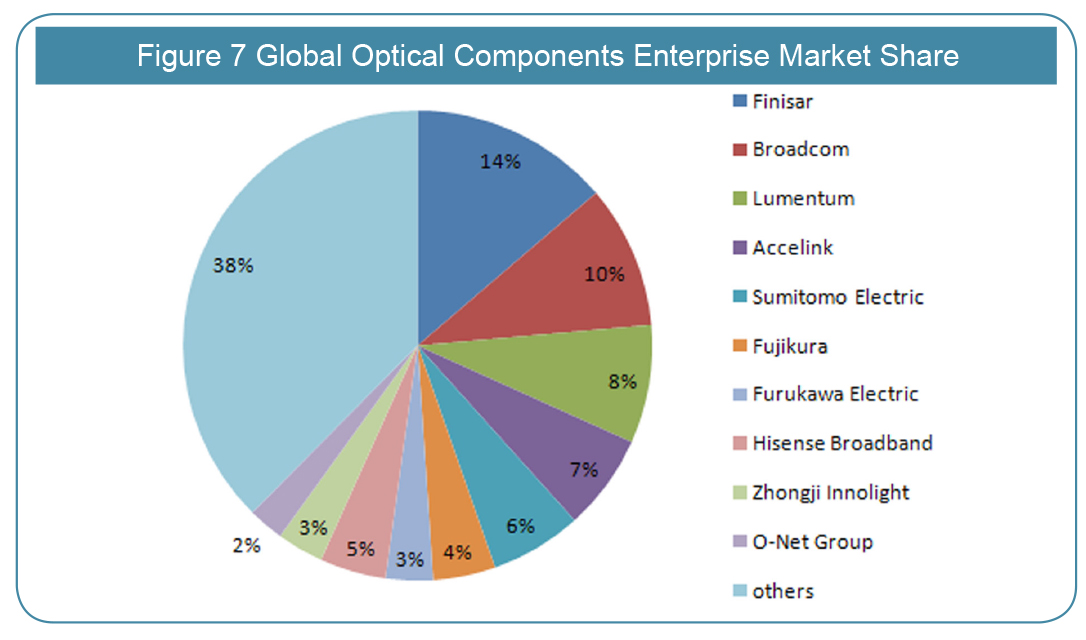

Optical communication components technology is necessary and strategic with perspectiveness, pioneer, and exploration in optical fiber communication industry, which shows a country’s technological innovation capability in optical fiber communication technology field. It is worth mentioning that among the top 10 optical components manufacturers in the world, three are from the United States, three are from Japan, and the remaining four are from China. This proves that Chinese companies have made great progress in the field of optical components and are narrowing the gap with United States and Japan. Accelink is still in fourth place this year, the same ranking as last year, while Hisense Broadband Multimedia, Zhongji Innolight and O-NET ranks 8th, 9th and 10th, respectively. Finisar, Broadcom and Lumentum score 1000, 995 and 977, respectively, in the top three, with little difference in competitiveness. In terms of market share, First-ranked Finisar occupies 14% of the market share, while the second and third places of Broadcom and Lumentum are 10% and 8%, respectively; the fourth Accelink’s market share is 7 percent; the remaining three Chinese enterprises Hisense Broadband Multimedia, Zhongji Innolight and O-NET rank 8th, 9th and 10th with 5 percent, 3 percent and 2 percent market share, respectively, while Sumitomo Electric, Fujikura and Furukawa Electric have market shares of 6 percent, 4 percent and 3 percent, respectively. These ten enterprises account for 62% of the optical components market.

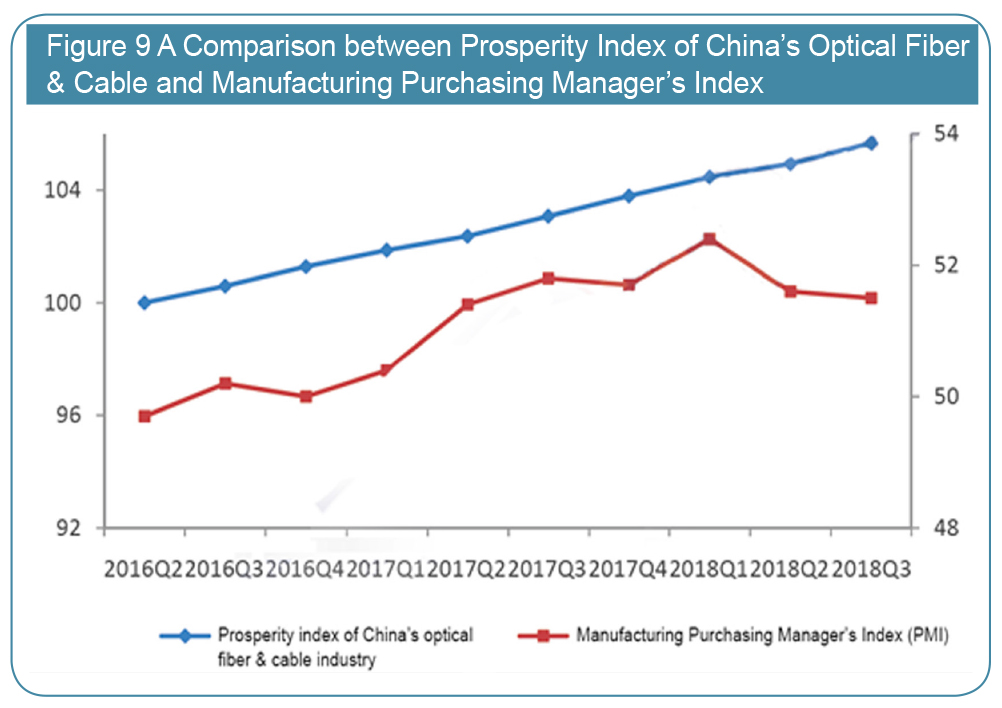

The trend of coordinate development is more and more evident between the network infrastructure optical fiber & cable industry and entity economy. China’s Purchasing Manager’s Index (PMI) is usually regarded as a good sign of entity economy to measure the conditions of China’s manufacturing sector in production, new orders, products price, inventory, employees, order to deliver (OTD), new export orders as well as imports. Figure 5 shows that prosperity index of optical fiber & cable industry has existed an obvious positive correlation with Purchasing Manager’s Index from the second quarter in 2016 to the third quarter in 2018. Optical fiber & cable industry grows steadily, and the growth of entity economy is more evident, both of which generally have a positive trend, and the correlation coefficient is about 0.86. Therefore the trend of coordinate development is more and more evident between the optical fiber & cable industry and entity economy.

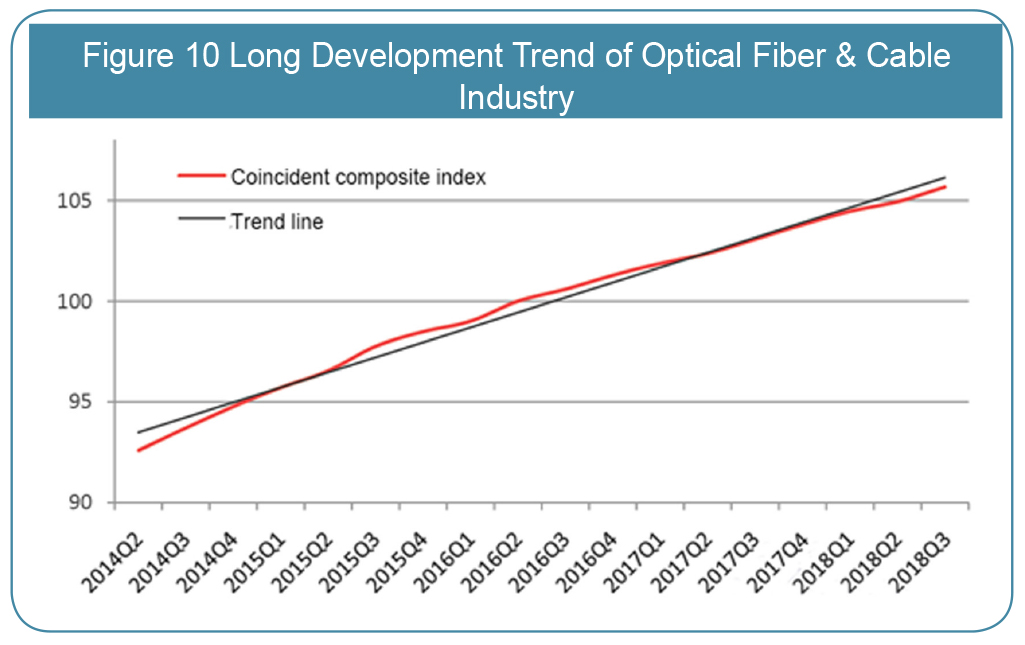

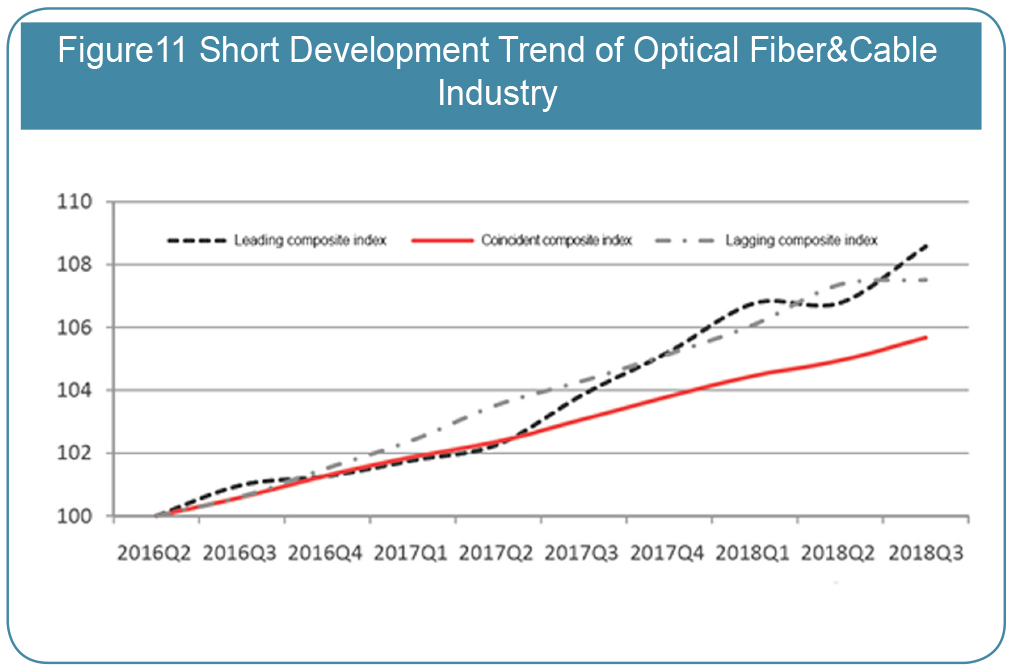

Trend analysis of prosperity index 1. Analysis of coincident index

In the short term, coincident index grows steadily in the latest quarters. From the fourth quarter in 2017 to the third quarter in 2018, coincident index is respectively 103.81, 104.48, 104.95, and 105.68, increasing by 0.71, 0.66, 0.47, and 0.72 on quarter to quarter. The steady growth of coincident index demonstrates that China’s optical fiber & cable industry generally keeps a positive development trend.

2. Analysis of leading index

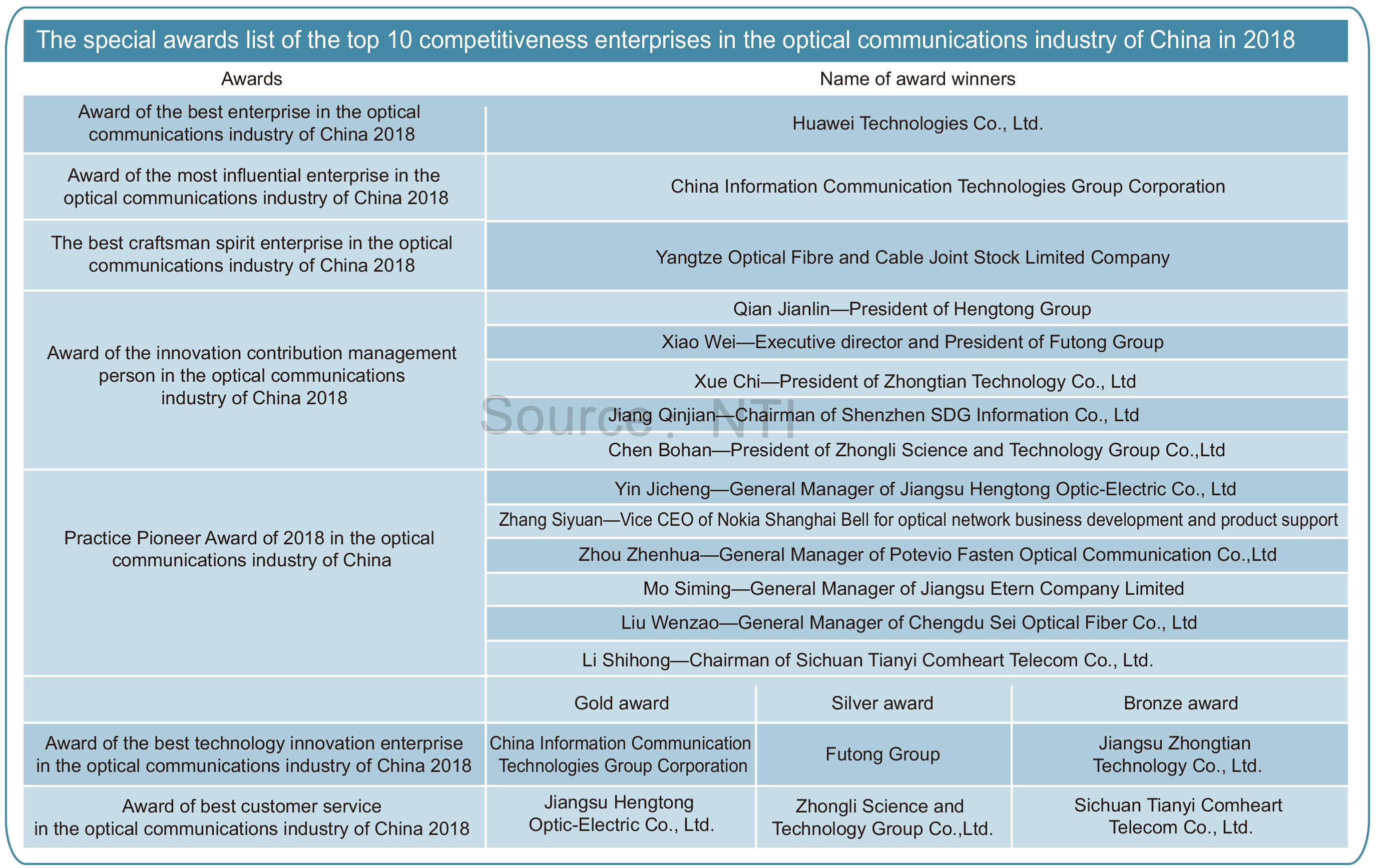

In the end, I’m honored to express my sincere gratitude to all partners in optical communication industry for their long-term help and support on behalf of all staffs of “ The Annual Top 10 Competitiveness Enterprises in the China/Global Optical Communication Field ”. Thank you!

|

Ranking of "The Top 10 Competitiveness Enterprises in the Optical Communications Industry of China & Global market in 2018" |

|||||||

|